ESRS vs CSRD: what’s the difference, how ESRS is changing and how to meet the new requirements

The practice of reporting sustainability data has exploded in recent years and is now expected from all but the smallest companies. But it can feel like the Wild West, with a dizzying array of standards, frameworks, and systems.

The European Sustainability Reporting Standards (ESRS) are designed to align everyone to one set of reporting rules and significantly raise the bar on data quality.

What is the ESRS, and how does it relate to the CSRD?

The ESRS are the detailed reporting guidelines for how companies subject to the Corporate Sustainability Reporting Directive (CSRD) need to report their sustainability data. The aim is to improve the quality and comparability of sustainability reporting.

In simple terms, the CSRD is the ‘what’ and the ‘why’, and the ESRS is the ‘how’.

Updates to the ESRS from the Omnibus Simplification Package

If you feel like sustainability reporting compliance is a headache, you’re not the only one. The EU is working to make it easier, in response to market feedback.

On 26 February 2025, the EU Commission released its Omnibus Simplification Package, which proposes changes to simplify the CSRD, EU Taxonomy, and other related regulations and reduce the number of companies in scope. The aim is to improve Europe’s business competitiveness by reducing time spent on reporting, while still supporting climate goals.

The proposals are making their way through the EU’s lengthy legislative process, so there won’t be a final agreement for a while, likely early 2026.

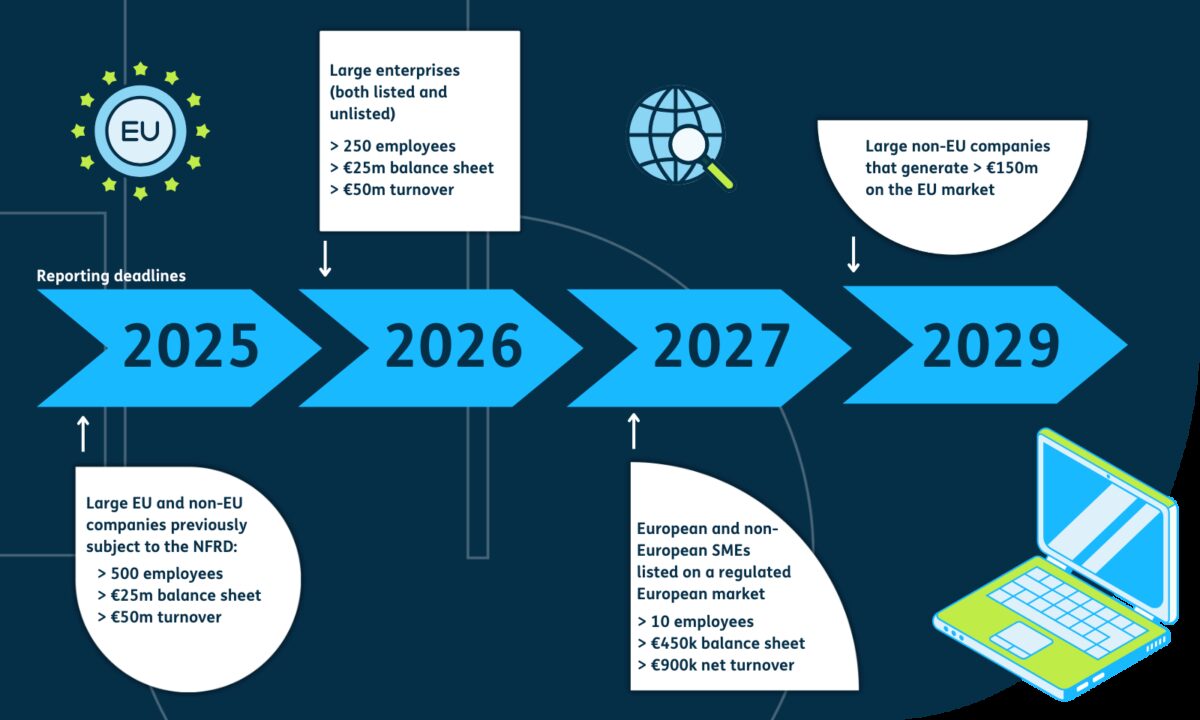

While things are in flux, the ‘stop-the-clock’ directive has been agreed.

This means that for most companies (all except the first wave of large companies that already started preparing CSRD reports), they won’t need to start reporting until 1 January 2028.

And the ESRS is being updated, aiming to:

- Remove some of the mandatory datapoints that are deemed least important for general sustainability reporting

- Improve alignment between the CSRD and other EU regulations and global standards such as the TCFD

- Clarify the guidelines

- Provide better guidance on double materiality to ensure companies are only reporting the most material datapoints and don’t spend unnecessarily long on the materiality assessment itself

The EU Commission has asked the European Financial Reporting Advisory Group (EFRAG - yep, another acronym!) to put together technical advice on how to simplify and update the ESRS, due by 31 October 2025.

While the final form of the ESRS is uncertain, let’s familiarise ourselves with the current draft and why it matters to your business.

Who does the ESRS apply to?

The ESRS applies to the same companies subject to the CSRD: large and listed companies based in the EU and those based elsewhere - including the UK - if they have a net turnover of over 150 million euros per year in the European market.

Why the ESRS matters

If you are subject to the CSRD, ensuring your sustainability reporting aligns with the ESRS is a legal requirement.

Beyond compliance, the benefit for business is that more relevant and high-quality sustainability data can feed back into your strategy and give you greater insight into your risks, opportunities, impacts, and progress.

For stakeholders, the benefit is improved transparency. Specifically, more accurate data that is more comparable to other companies. The goal is to elevate sustainability reporting to the standard we expect from financial reporting.

Breakdown of the different ESRS standards: topics and subtopics

So, what exactly are these standards? Keep in mind, the ESRS is not finalised and that the Simplification Omnibus Package may limit the mandatory elements.

Currently, the ESRS includes:

- 2 cross-cutting standards that are mandatory for all companies. These are ‘General Requirements’ (ESRS 1) which cover general principles for reporting and ‘General Disclosures’ (ESRS 2) which state what needs to be covered for each topical standard that is material to the company.

- 10 topical standards which are subject to a materiality assessment.

There will also be sector-specific standards, due to be adopted on 30 June 2026.

The 10 topical standards are broken up into 5 environmental topics, 4 social topics, and 1 governance topic:

🌍 Climate change (ESRS E1)

🛢️ Pollution (ESRS E2)

🌊 Water and marine resources (ESRS E3)

🌿 Biodiversity and ecosystems (ESRS E4)

♻️ Circular economy (ESRS E5)

👷♀️ Own workforce (ESRS S1)

🔗 Workers in the value chain (ESRS S2)

🏘️ Affected communities (ESRS S3)

🛍️ Consumers and end-users (ESRS S4)

🏛️ Business conduct (ESRS G1)

Each topic also has several subtopics - here's the full list. For each topical standard, you need to apply the ESRS 2. So, that means covering how it fits into your governance and strategy, and how you manage impacts, risks, and opportunities. For each topic, your reporting will need to include a written narrative explanation as well as hard data. (The proposed upcoming changes to the ESRS are likely to focus more on quantitative data.)

3 tips for ESRS success

Depending on how sophisticated your sustainability reporting already is, complying with the ESRS could be a matter of tweaking your current reporting process or a mammoth overhaul. Here are our tips for success:

- Make sure you have a team in place for data collection. The breadth and depth of data required is extensive, and you will also need data from your suppliers. Make sure you have properly resourced this function. Ensure everyone has had training on the ESRS requirements and reporting tools, and that you have a clear delegation of roles and responsibilities.

- Documenting your methodology for assurance. Under current rules, you are required to undergo an external audit with limited assurance from the first year of reporting under the CSRD. This means it’s essential to record your process and methodology.

- Improve your process each year. In your first year of reporting, things won’t be perfect. The important thing is to set a baseline and improve your reporting capability year-on-year. Just as the underlying sustainability action you’re reporting is a journey, so is your reporting.

What the final report looks like

According to the CSRD, you need to integrate your sustainability data into your financial annual report by including a sustainability statement in the management review section.

This means instead of having both a financial report and a sustainability report, you could have just one big report that provides a holistic view of your performance and value creation. For example, the renewable energy company Orsted published a comprehensive 2023 annual report that aligns with the ESRS, including a detailed account of its double materiality assessment and information on its material ESG topics.

How we can help

If this looks overwhelming, remember two things.

Firstly, you only need to report on the topics that are material to your business, not the whole set.

Secondly, we are here if you need a helping hand. Our expert team can support you with:

- Making sense of regulatory requirements

- Double materiality assessment to determine which topics you need to report on

- Gap analysis between your current reporting and ESRS

- Data point collection

- Developing your report

Our consultants have supported many companies with their sustainability strategies and reporting, including working with Kingfisher group (B&Q and ScrewFix) for over 10 years. Learn more about our CSRD support package here.

Subscribe to our newsletter for future updates on the ESRS and CSRD regulation.

We're here to help

- 30 years of experience at the forefront of corporate sustainability

- Award-winning, innovative solutions

- A trusted partner: as a charity, we reinvest our profits to create change

Discover our CSRD & ESRS support package

Learn more